Deal funded

26-Unit New-Build Refinance in Texas

Refinancing a New Construction Portfolio Without Stabilized Income

portfolio

26 Units

product

DSCR Refinance

LOAN AMOUNT

$2,300,000

Term

30 Years

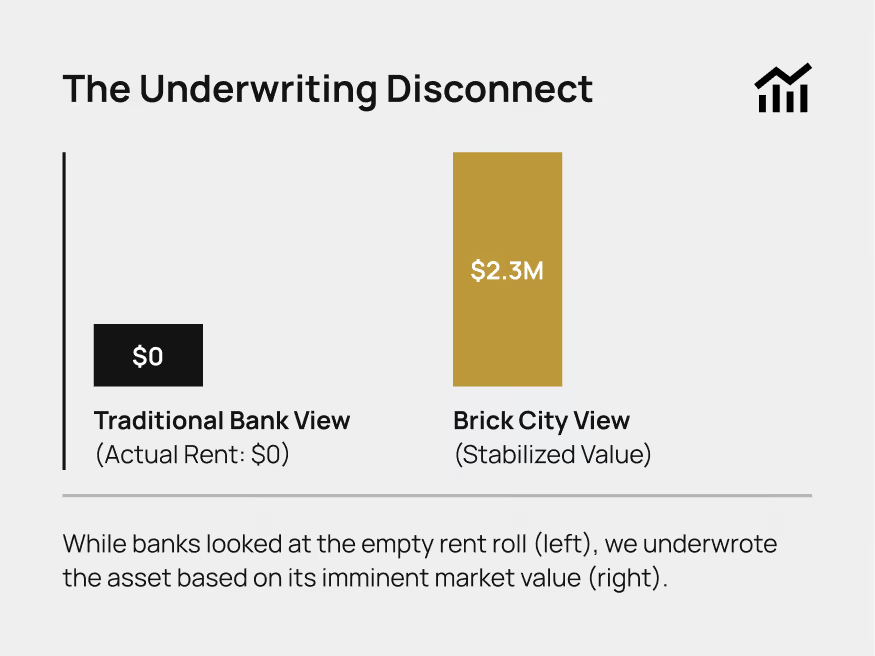

The borrower had successfully delivered 26 units in a desirable Houston submarket, but timing was critical. The construction loan was maturing, yet the property was physically complete but operationally empty. Lease-up had barely begun, creating a disconnect between the asset's value and its current income.

While banks looked at the empty rent roll (left), we underwrote the asset based on its imminent market value (right).

For most lenders, this combination results in an automatic decline. Traditional banks require a "seasoning" period—usually 90 days of 90% occupancy—before they will refinance construction debt. With the loan maturity approaching, the borrower didn't have the runway to stabilize.

Wait for 90% occupancy and 3-6 months of seasoning on the rent roll.

Result: Borrower defaults on construction loan maturity.

Underwrite based on market-supported rents and asset quality, not historical collections.

Result: Loan closes in 30 days.

1

We utilized stabilized rent projections from the appraisal rather than the empty rent roll, validating rates via comps.

2

Consolidated underwriting for all 26 units into a single operating model, saving roughly 2 weeks of processing time.

3

Loan funded ahead of maturity, providing the borrower a 30-year runway to lease up at their own pace.

"We didn't wait for the asset to stabilize. We built the model it was moving toward and delivered capital on that basis. If you size this on in-place numbers, there is no loan."

Our headquarters

50 Park Place, Suite 301

Newark, NJ 07102

loan products