.avif)

The borrower, an active investor and entrepreneur, owned several Miami investment properties financed through a private lender. The existing financing had reached a maturity deadline, creating urgency to refinance the portfolio and retire the outstanding private debt.

Beyond the refinance itself, the borrower’s goal was to unlock additional capital from the portfolio to support business expansion. To accomplish both objectives, the transaction needed to:

Pay off the existing private lender

Maintain leverage across multiple property types

Generate meaningful cash-out proceeds

By the time the deal closed, the borrower had achieved just under $1M in net cash-out proceeds while consolidating the portfolio into long-term financing.

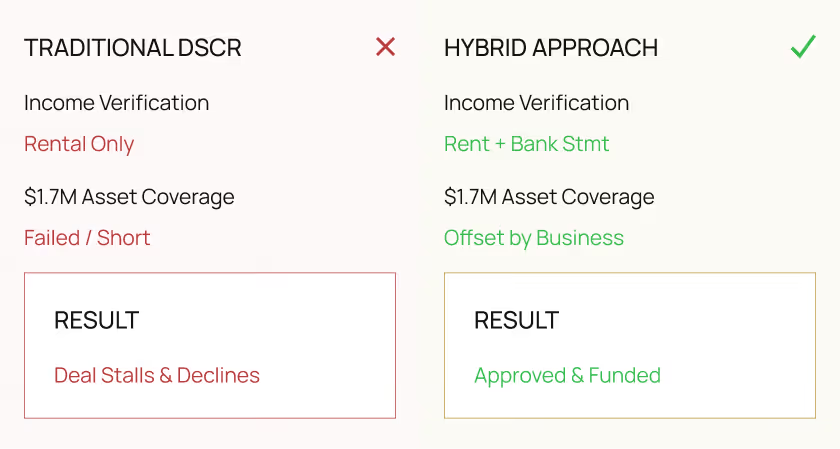

On the surface, the deal appeared to fit within standard DSCR lending parameters. But once underwriting began, several structural complications emerged. The portfolio contained multiple property classifications, including a luxury non-warrantable condo, a single-family property with an additional dwelling unit (ADU), a property sitting on more than five acres, and assets with low appraised rental income relative to property value.

One property in particular highlighted the problem. Despite being valued at $1.7M, the appraisal supported only $3,700 per month in rental income. Under a traditional DSCR model, that level of rent could not support the debt service required for the desired loan amount. The issue wasn’t the borrower’s financial strength, it was the rigidity of traditional underwriting.

Multiple property types, appraisal complications, or income limitations can cause otherwise strong deals to stall. Pre-flight your scenario and our team will evaluate structure before underwriting begins.

Rather than forcing the deal into a traditional DSCR framework, the team restructured the transaction mid-process. The solution was a hybrid DSCR + bank statement qualification approach. This allowed the underwriting model to evaluate two income sources simultaneously:

Rental income generated directly from the properties

Verified business income through bank statements

Using this hybrid approach accomplished two critical things. First, it supplemented debt coverage for the properties that underperformed strictly on rental income. Second, it allowed the borrower to qualify without submitting tax returns, maintaining the flexibility that investor borrowers often require.

At the same time, the team worked through appraisal concerns. Because one property had been classified as a unique asset with distant comparable sales, the valuation initially created eligibility issues. By facilitating an amended appraisal review, the property was reclassified and made eligible within the lending framework. Once these adjustments were made, the portfolio could move forward toward closing.

With the revised structure in place, the portfolio was approved quickly after a full file submission. Within seven days of receiving the completed package, the loan received approval and moved toward closing.

Loan Amount

$2,787,000

Property Type

4 Miami Investment Properties

Structure

Hybrid DSCR + Bank Statement

LTV

65%

Private debt retired and nearly $1M in cash-out proceeds generated, closing without the need for tax returns while maintaining leverage across all four properties.

What began as a traditional DSCR refinance ultimately required a creative hybrid solution to align the borrower’s income profile with the realities of the assets.

Our headquarters

50 Park Place, Suite 301

Newark, NJ 07102

assets

assets

Our HeadQuarters

50 Park Place, Suite 301 Newark, NJ 07102

Contact

sales@brkcty.com

* Lorem ipsum dolor sit amet. Lorem ipsum dolor sit amet. Lorem ipsum dolor sit amet. Lorem ipsum dolor sit amet. Lorem ipsum dolor sit amet. Lorem ipsum dolor sit amet. Lorem ipsum dolor sit amet. Lorem ipsum dolor sit amet. Lorem ipsum dolor sit amet. Lorem ipsum dolor sit amet. Lorem ipsum dolor sit amet. Lorem ipsum dolor sit amet. Lorem ipsum dolor sit amet. Lorem ipsum dolor sit amet. Lorem ipsum dolor sit amet. Lorem ipsum dolor sit amet. Lorem ipsum dolor sit amet. Lorem ipsum dolor sit amet. Lorem ipsum dolor sit amet. Lorem ipsum dolor sit amet. Lorem ipsum dolor sit amet.

Disclaimers: