Wait for 90% occupancy and 3-6 months of seasoning on the rent roll.

Result: Borrower defaults on construction loan maturity.

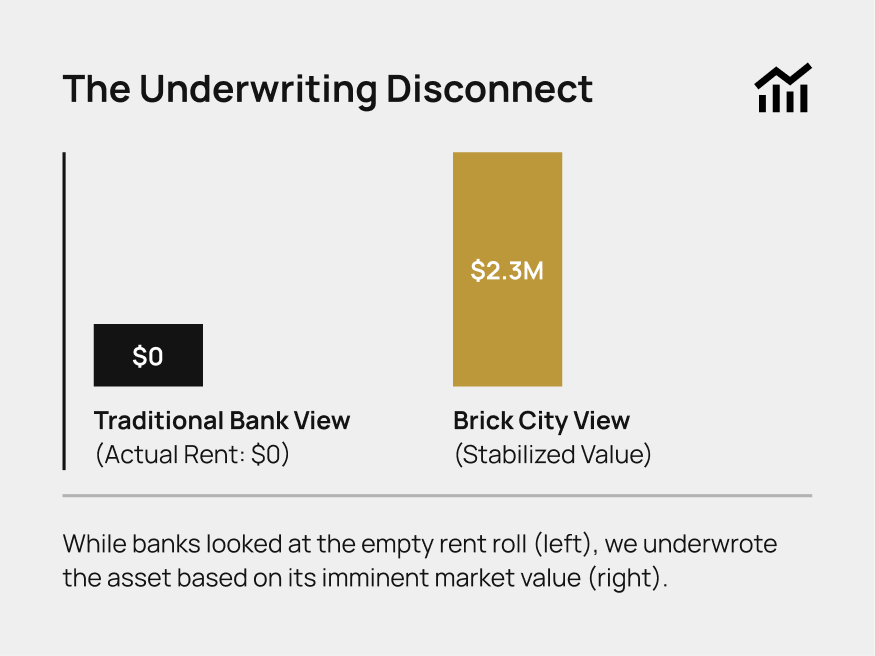

Underwrite based on market-supported rents and asset quality, not historical collections.

Result: Loan closes in 30 days.

.png)

Brick City Capital specializes in DSCR financing for investors who value certainty.

Our headquarters

50 Park Place, Suite 301

Newark, NJ 07102

assets

assets

Our HeadQuarters

50 Park Place, Suite 301 Newark, NJ 07102

Contact

sales@brkcty.com

* Lorem ipsum dolor sit amet. Lorem ipsum dolor sit amet. Lorem ipsum dolor sit amet. Lorem ipsum dolor sit amet. Lorem ipsum dolor sit amet. Lorem ipsum dolor sit amet. Lorem ipsum dolor sit amet. Lorem ipsum dolor sit amet. Lorem ipsum dolor sit amet. Lorem ipsum dolor sit amet. Lorem ipsum dolor sit amet. Lorem ipsum dolor sit amet. Lorem ipsum dolor sit amet. Lorem ipsum dolor sit amet. Lorem ipsum dolor sit amet. Lorem ipsum dolor sit amet. Lorem ipsum dolor sit amet. Lorem ipsum dolor sit amet. Lorem ipsum dolor sit amet. Lorem ipsum dolor sit amet. Lorem ipsum dolor sit amet.

Disclaimers: